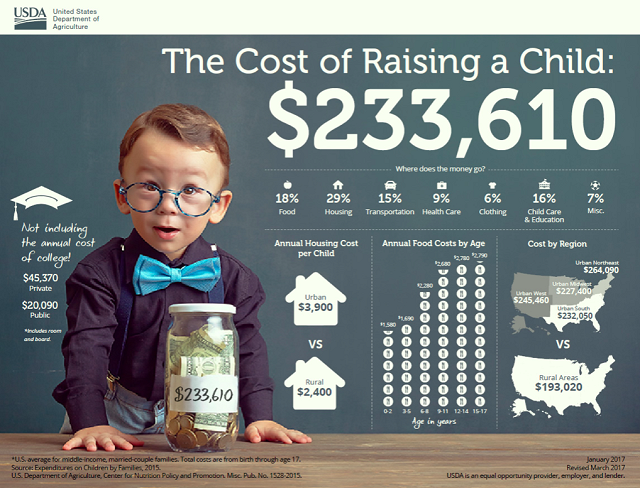

Becky and I never had children. As far as we know, we could have, but between having careers we enjoyed, my ambivalence towards having them, and our combined procrastination, we never did. Financially, it was a good move. Almost all of you have children at this point, who we love, but also recognize the associated financial burden. That said, Becky and I always lived below our means.

For me, I think this came from my parents, which came from my grandparents. Particularly on my mother’s side, my grandparents told stories of living through the Great Depression and they never really got out of that mindset. Grandpa Murphy, at 90+ years old, had a job working at the civic center in Lakeland, Florida during the winter. At 90, he was still having 401(k) dollars held from his check because he wasn’t going to turn down the employer match! Ha!

I never received an allowance, but when I received money for Christmas or when I turned 12 and started mowing yards, mom made me save half of what I earned. When I got into high school, I was on a mowing crew that mowed yards and picked up leaves at houses around Lake Maxinkuckee. I still saved that half “for college”. It was somewhat ingrained, so when I got my first job out of college, I wrote checks to invest in mutual funds at the end of each month. I didn’t manage to continue 50%, but I still did it. The first time I got a bonus, I considered that “found money” and 100% of that was invested. I still own those stocks. (Compaq became Hewlett Packard, which became two different Hewlett Packard companies…)

Becky was more altruistic than me. She got a degree in education and took a teaching job, which barely covered her expenses. In her first professional job in Arkansas, she lived on dried beans with powdered flavoring. When we moved in together, she contributed what she could and since our combined expenses were not much more than what my base expenses were, most of that boosted the monthly savings I was doing. When we got married, she was unhappy with the teaching job and wanted to go back to get a Masters in Audiology, so she could change careers. To accelerate that, she didn’t work while going to school. We lived on my salary during that period, bought a house and while savings were reduced, we still continued to save. (Part of that savings was additional principal payments on the house, but I’ll talk more about that later.)

Investing in Becky’s Degree was one of my best investments. She was immediately happier and right out of school, she got a job that paid better than mine. Since we had been living on just my salary, we mostly continued to do so. At that time we moved back to Indiana. Since ECC is a family business, I was limited in what I could contribute to my 401(k) per IRS rules (I was a highly compensated employee in theory, though I had no ownership and several employees made more than I did and they didn’t meet that designation!), but we maxed out contributions to Becky’s 401(k) and we contributed to IRAs on the side. Becky had access to an FSA through her employer and we used that too. Later, we became eligible for HSAs and we have maxed them out as well, while continuing to pay medical bills out of pocket. When 401(k) catch-up contributions were allowed, we maxed those out too. When Roth IRA’s became a thing, we switched to them.

Not everyone can do this. As I started this, I fully understand the impact children have on finances. Just the day-to-day is daunting without adding in the cost of college or other things to move them out of the nest. (If you’re able to do so!) But part of the parenting responsibility is not to be a burden on your children. Retirement may well last for 30+ years. Living below your means lets you save and invest for when that day comes. In our case, our life decisions meant we don’t have children as a safety net in our old age. We better have saved well!